Investing at All-Time Highs

When markets reach new highs, investors often feel pressure to do something—buy more, sell, move to cash, or make a dramatic portfolio change. Many investors begin to feel uneasy. This is understandable, as it’s a natural human instinct to worry.

After all, buying when markets are setting records can feel uncomfortable. Many investors may feel they're arriving at the party just as it's ending. For retirees and those approaching retirement, the stakes can feel even higher because preserving wealth is just as important as growing it.

Before making any investment decisions based on recent market highs, it's helpful to put those highs into historical context.

All-Time Highs Are Normal

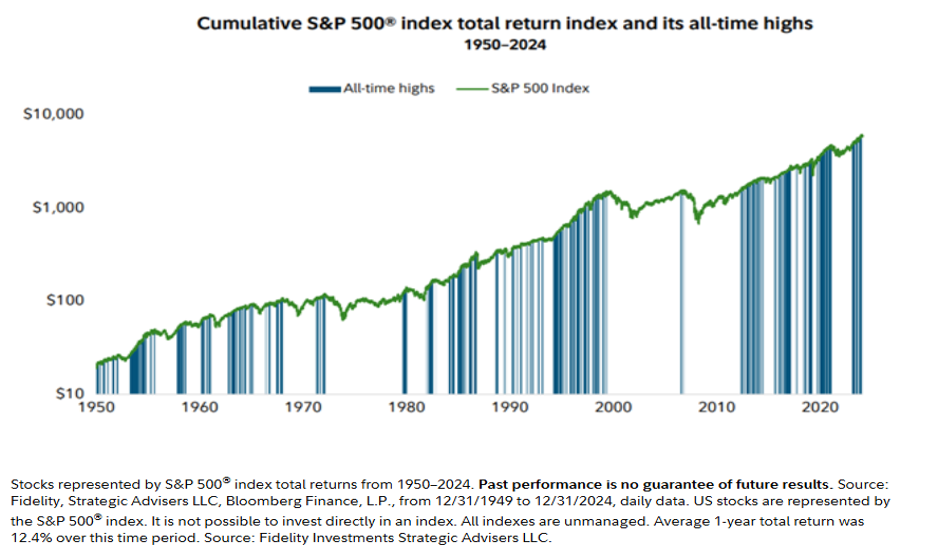

First, we should remind our readers that markets frequently hit new highs (see chart below). There is nothing new about this fact. Market records certainly make good headlines for the financial news media but again they are not rare events. As seen below, consider the S&P 500, which has reached dozens of new all-time highs over the decades. Put differently, if markets didn’t regularly set new records, it would mean the businesses are not growing, innovating, and generating profits. New highs occur regularly. It’s a basic feature of long-term investing.

Of course, investing at all-time highs doesn’t come without risk. There have been periods when markets traded at higher-than-average valuations, which can lead to increased volatility, including potential corrections (declines of 10% or more). However, elevated valuations alone have not been reliable timing tools for investors as history shows that markets have always recovered from downturns, even from much steeper bear markets, provided you stayed invested and diversified.

Time in the Market Matters More Than Timing the Market

Many investors attempt to wait for the "perfect" entry point. The challenge is that market declines are impossible to predict consistently. Often, periods following new highs are followed by even higher highs. The markets don't operate on a specific schedule. A market that reaches a new high today can continue climbing for months or even years. Likewise, a market that appears expensive can become even more expensive before eventually experiencing a correction.

Missing just a handful of strong market days can significantly impact long-term investment results and potentially hurt wealth. According to data, of the 1,188 months since January 1926, the market was at an all-time high in 363 of them, or 31% of the time. And get this. On average, 12-month returns following an all-time high being hit have been better than at other times: 10.4% compared with 8.8% when the market wasn’t at a high (see chart below). Returns on a two- or three-year horizon have been similar, regardless of whether the market was at an all-time high or not.

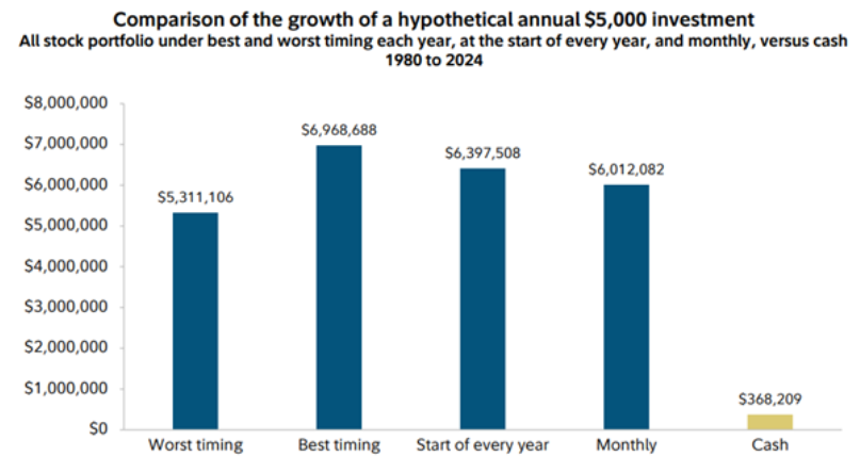

For retirees and long-term investors, staying invested has historically been a successful strategy than trying to predict short-term market movements. Even professional investors struggle to consistently predict short-term market movements. For individual investors, the challenge is even greater. In fact, if investors avoided investing every time the market reached a record level, they would have missed many years of strong returns (see chart below).

Stock returns represented by the S&P 500® index from January 1,1980–December 31, 2024. Past performance is not a guarantee of future results. Source: Fidelity, Asset Allocation Research Team, Bloomberg as of 12/31/24. The hypothetical example assumes an investment that tracks the returns of the S&P 500® Index and includes dividend reinvestment but does not reflect the impact of taxes, which would lower these figures. “Best days” were determined by using the one-day total returns for the S&P 500® Index within this time period and ranking them from highest to lowest. There is volatility in the market and a sale at any point in time could result in a gain or loss. Your own investment experience will differ, including the possibility of losing money. It is not possible to invest directly in an index. All indexes are unmanaged.

If your investment portfolio is appropriately diversified and aligned with your goals, objectives and risk tolerance, a new market high should not necessarily change your long-term strategy. Whether markets are at record highs or are experiencing temporary declines, maintaining discipline is often one of the most valuable decisions an investor can make.

Staying Focused on What You Can Control

What investors can control are the factors that may matter most:

• Maintaining a diversified portfolio.

• Keeping investment costs reasonable.

• Managing taxes thoughtfully.

• Rebalancing when appropriate.

• Staying aligned with long-term goals.

• Avoiding emotional decisions.

For investors saving for retirement, generating income, or preserving wealth for future generations, the answer often depends less on today's market level and more on having a thoughtful, well-constructed financial plan.

For retirees, the discussion is a bit different than it is for younger investors. While the principles of long-term investing apply to all investors, retirees often face additional considerations because their portfolios may need to support current income needs as well as long-term growth.

Retirement portfolios have multiple objectives:

• Generating income.

• Preserving purchasing power.

• Managing risk.

• Supporting long-term financial goals.

Because of these priorities, the decision isn't usually about investing everything into stocks at once or avoiding the market altogether.

Instead, retirees may benefit from focusing on questions such as:

• Is my portfolio appropriately diversified?

• Am I taking more risk than necessary?

• Do I have sufficient cash reserves for near-term spending needs?

• Does my investment allocation still reflect my goals?

These questions are generally more productive than trying to predict the market's next move.

The Bottom Line: A Financial Plan Matters More Than a Market Headline

History suggests that long-term investors can potentially be rewarded for staying invested and remaining focused on their goals rather than reacting to short-term market concerns.

If you have a diversified portfolio designed for income and growth, trust your plan. This means stocks for growth, bonds for stability, and cash for short-term needs.

Ask yourself:

Am I diversified across different asset classes?

Do I have enough liquidity for near-term spending?

Can I sleep well at night with my current level of investment risk?

If the answer to these questions is yes, then the right move may be to stay the course. If you’re unsure or feel uncomfortable, review your financial plan with your advisor—not because the market is at a record high, but to ensure your plan still matches your goals and circumstances.

The views stated in this letter are not necessarily the opinion of Cetera Wealth Services, LLC and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results. All investing involves risk, including the possible loss of principal. There is no assurance that any investment strategy will be successful. A diversified & allocated portfolio cannot eliminate the risk or guarantee a profit or protect you from loss.

- fidelity.com/learning-center/wealth-management-insights/stocks-at-all-time-highs

- hartfordfunds.com/insights/market-perspectives/equity/scared-of-investing-as-stocks-hit-all-time-highs-do-not-be.html